[ad_1]

I should be getting outdated.

Know the way I do know? Associates of mine don’t ship me new music lately. They simply ship me viral movies.

At present thus far, I’ve snickered, mesmerized, ooh, maybe 31 occasions at Democracy Manifest Man.

The opposite video hyperlink I’ve acquired? Robert Plant performing Stairway To Heaven, for the primary time in 16 years, within the comparatively teeny venue of Soho Farmhouse (UK).

The gang in that video certainly is aware of, all the way down to their bones, that they need to be stood in hushed reverence. In spite of everything, they is perhaps witnessing the final ever time that King Zep, 75, performs his most universally cherished track aloud.

However have you learnt what some individuals in that crowd do? They really sing alongside. Misplaced within the second, they tunelessly echo again Plant’s phrases, slightly than basking in them. They will’t assist themselves.

Watching this tableau – individuals giddily parroting a scintillating refrain, regardless of how inapposite doing so may appear in hindsight – jogged my memory a bit little bit of the music trade and Merck Mercuriadis.

Over the previous month, I’ve listened to a number of, let’s say, Mercuriadis skeptics (he’s on various rivals’ dartboards, that man!).

Usually with some glee of their voices, these of us have daydreamed aloud how Hipgnosis Songs Fund‘s ‘continuation vote’ will turn out to be the second their imaginary nemesis lastly will get nobbled.

“It’s the day the home of playing cards lastly falls down! The day the piper will get paid! The day Merck’s left ‘holding the bag’!” and many others.

Effectively, as you most likely know by now, that ‘continuation vote’ came about yesterday morning in London (October 26).

It was anticipated {that a} cheap majority of Hipgnosis Songs Fund (HSF) shareholders, annoyed by the agency’s sagging share worth and the shock latest slashing of their interim dividend, would vote in opposition to continuation.

This, although, was a landslide: Round 83% of HSF stockholders opted to reject ‘continuation’ – whereas additionally voting to instantly oust HSF’s already-exiting Chairman, Andrew Sutch.

The transfer has left the way forward for HSF hanging within the stability.

But removed from spelling the tip of Merck Mercuriadis (and the Blackstone-backed funding adviser he leads, Hignosis Tune Administration), Hipgnosis Songs Fund’s ‘discontinuation’ might but play proper into his palms.

In a second, I’m going to do a spot of my very own “giddy parroting”, by paraphrasing in textual content some conversations I’ve had (and never had) with individuals this previous fortnight about Mercuriadis and HSF, and their respective futures.

However for now, let’s hear from the person the entire trade’s speaking about (once more!)… through a press release that Mercuriadis issued within the wake of the discontinuation vote from HSF shareholders.

“[Yesterday’s] Hipgnosis Songs Fund AGM marks a chance to reset and give attention to the long run. Our conversations with shareholders have revealed a consensus that they’re enthusiastic concerning the high quality of [HSF’s] iconic portfolio of songs.

“Nevertheless additionally it is clear that they’re asking for change and we respect that suggestions. Hipgnosis Tune Administration’s new administration workforce and I’ve already began taking the related essential motion to satisfy the expectations of shareholders.

“Our dedication to the Firm’s shareholders stays absolute and we stay up for working with a brand new Chair and reconstituted Board throughout this era to make sure that the Hipgnosis Songs Fund delivers for its shareholders. Throughout this course of, shareholders will be sure that Hipgnosis Tune Administration will proceed to handle the Songs with the best responsibility of care as all the time.”

Mercuriadis additionally thanked Andrew Sutch, in addition to non-exec administrators, Andrew Wilkinson and Paul Burger – who each fell on their swords forward of yesterday’s vote – for his or her service.

So: what occurs now? Is Mercuriadis actually fried? And the way on earth can it’s potential, post-HSF’s discontinuation, that he’s left “holding all of the playing cards”?

To clarify, take pleasure in this author arguing with himself in eight simple steps…

Step 1: What a thumping loss for Merck! 83%! Does he now get ousted?

Not the neatest begin to this dialog.

A ‘continuation vote’ – which all funding trusts on the London Inventory Alternate legally have to carry each 5 years – doesn’t imply the rapid finish of a fund. Nor does it imply the rapid finish of that fund’s relationship with its funding adviser.

Yesterday, in a word to traders, JP Morgan’s Christopher Brown succinctly summarised what discontinuation really means for HSF:

“In accordance with [HSF’s] prospectus, the Board is now required to place ahead inside six months proposals for the reconstruction, reorganisation or winding-up of [HSF]. These proposals might or might not contain winding-up [HSF] or liquidating all or a part of the present portfolio of investments.”

In the meanwhile, HSF is sustaining its funding adviser – Hipgnosis Tune Administration (HSM) aka Merck Mercuriadis. In the meantime, yesterday HSF shareholders re-elected three of the corporate’s Board Administrators: Simon Holden, Sylvia Coleman and Cindy Rampersaud.

In order you learn this, HSF nonetheless has a board, and nonetheless has an funding adviser.

Probably the most urgent concern of that board? Discovering a Chairman to switch the now-ousted Andrew Sutch.

Rumors recommend {that a} seemingly candidate to fill these footwear will likely be Rob Naylor, beforehand the Chairman of Round Hill‘s UK royalty fund (which is able to shortly be the property of Concord).

Related: clearly, Hipgnosis Tune Administration (aka Mercuriadis and his workforce) additionally counts Blackstone-backed Hipgnosis Tune Capital (HSC) as a shopper.

So even when HSF did handle as well him out – which I doubt will occur, as I’m about to elucidate – Mercuriadis’s eggs aren’t multi functional basket anyway.

Step 2: Proper. however as soon as the brand new HSF board’s in place, they’ll both (a) Hearth Merck or (b) promote the corporate to another person – somebody like a serious music firm. He’s cooked!

Do you not learn Music Business Worldwide?

Sure, to be clear, the Hipgnosis Songs Fund board can now flip round – as they’ve all the time been in a position to do – and fireplace Hipgnosis Tune Administration as HSF’s adviser.

That’s unlikely, although not inconceivable, for a couple of causes.

Earlier this month MBW reported that Merck Mercuriadis had agreed to new concessions in HSM’s contract with HSF.

Even so, if HSF now fires HSM as its adviser, contractually HSM has a minimal 12-month discover interval; HSF would additionally need to pay HSM a further penalty.

Each of these items (the discover and the penalty), relying on the share worth, I hear, might add as much as someplace within the area of GBP £15 million to GBP £25 million.

After which, the killer element: As MBW reported last week, Hipgnosis Tune Administration and Merck Mercuriadis have an unique ‘name choice’ in place to purchase the whole thing of HSF’s property if HSM is ever terminated as HSF’s funding adviser (aka: if Mercuriadis is fired).

I’ll dig deeper into the solidity of that ‘name choice’ – and why it issues greater than you would possibly initially recognize – shortly.

A much bigger query for now: what does HSF firing HSM really acquire the listed firm within the quick time period? Apart from momentarily pumping some blood via the capillaries of HSF shareholders indignant concerning the present inventory worth?

As Mercuriadis mentioned in his assertion, HSF’s shareholders aren’t questioning the standard of the fund’s property – with stakes within the songbooks of Neil Younger, Shakira, Enrique Iglesias, 50 Cent, Lindsey Buckingham, Christine McVie, Jack Antonoff, Andrew Watt, and the Pink Scorching Chili Peppers, to call a handful.

Mercuaridis personally amassed this enviable portfolio for HSF, leaning on his distinctive contacts guide. He did so throughout 5 years (2018-2022) when – aside from a really small circle of others (hello Larry!) – Mercuriadis’ non-major-music-company rivals have been not often in a position to problem the scale of premium-level property that HSF swallowed up.

Sure, some will argue that Mercuriadis paid too excessive a a number of for sure property (whether or not newer catalogs or ‘classic’ catalogs).

However HSF shareholders clearly consider these catalogs have been price it: witness the actual fact they only rejected a $440 million supply from Blackstone/Hipgnosis Songs Capital (through Mercuriadis/HSM) for 29 of HSF’s catalogs… for a worth that represented a 26% premium on the unique price that Mercuriadis paid to accumulate them for HSF within the first place.

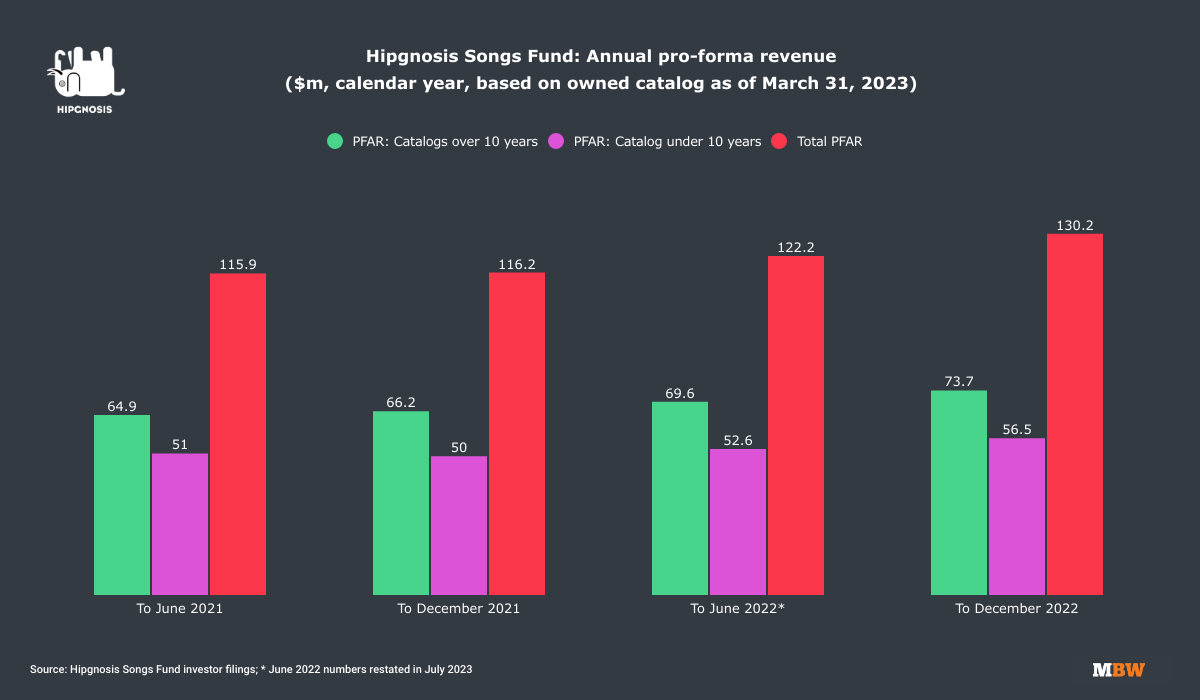

As well as, HSF’s top-line financials (earlier than focus shifted to the irritation of a halted October dividend and different board wobbles) look strong: In July, HSF introduced its strongest-ever annual fiscal outcomes, with like-for-like revenues up 10.9% YoY.

Final level: HSF shareholders will recognize that, by firing Mercuriadis, they invite the surface chance of a ‘Taylor Swift disaster’ – i.e. songwriters with whom Mercuriadis has struck offers (from Neil Younger, to Chrissie Hynde, The-Dream, the Chili Peppers, Lindsay Buckingham, Nile Rodgers et al) going public with potential anger over HSF making an attempt to separate Mercuriadis from repping their property.

Inevitably, such a state of affairs wouldn’t be nice information for HSF’s share worth.

Step 3: You’ve bought to confess, although, that every one of this HSF/HSC/HSM/Blackstone enterprise seems to be a bit nebulous…

Sure. There may be actually a good accusation to be made at Mercuriadis about battle of curiosity.

Since Hipgnosis Tune Administration started shopping for catalogs for Hipgnosis Songs Capital (i.e. with Blackstone’s money), HSF’s personal shopping for spree has floor to a halt.

To be clear: mentioned grinding to a halt has been brought on by HSF being “totally invested”. Whereas its shares commerce at a reduction the corporate is unable to elevate additional cash to purchase stuff – and it’s prudently not seeking to additional increase its credit score facility to take action in a high-interest setting.

However even when HSF did have a stack of recent capital to spend, its HSM relationship is inarguably difficult by HSC’s presence. (See: the main points of this 20% agreement between HSF and HSC).

HSF shareholders, within the harsh gentle of post-discontinuation, might not adore this complexity.

Step 4: In order that they WILL fireplace Merck!

No, I doubt they may… primarily as a result of his ‘name choice’ leaves HSF weak to acquisitive predation from Blackstone.

Have you ever seemed into the finer particulars of Mercuriadis’ ‘name choice’? I’ve.

It dates again to the prospectus of Hipgnosis Songs Fund, earlier than HSF floated in 2018 and earlier than any public shareholders invested a bean within the firm.

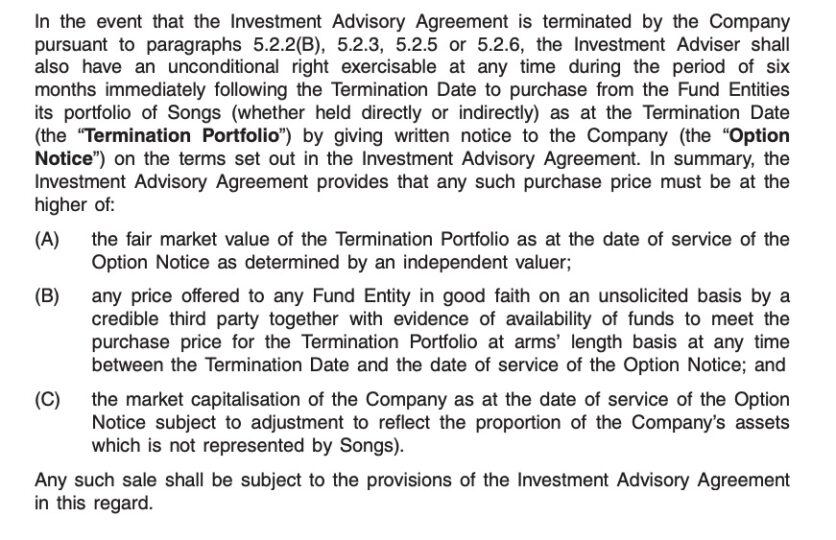

Under is a abstract of the ‘name choice’, from that prospectus, in black and white.

Observe: “[An] unconditional proper exercisable at any time throughout the interval of six months instantly following [HSM’s termination] to buy from the Fund… its portfolio of Songs (whether or not held straight or not directly).”

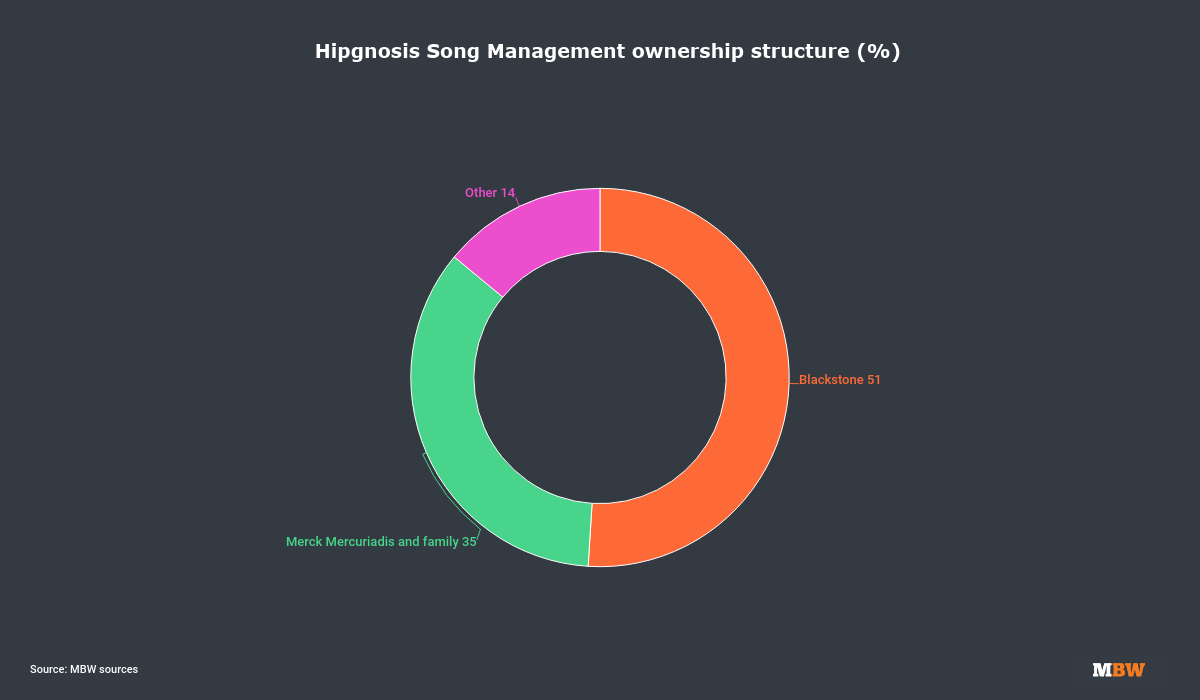

Hipgnosis Tune Administration (HSM) represents lots – as in, potential billions – of Blackstone {dollars} within the form of Hipgnosis Songs Capital (HSC).

Blackstone is strategically invested in Hipgnosis Tune Administration too, owning just north of 50% of the funding advisory firm.

In order quickly because the HSF board fires Mercuriadis, you may wager he’ll simply come and swipe their property, most likely utilizing Blackstone’s cash.

Or, if Blackstone for no matter purpose doesn’t have the urge for food for the deal, or is just prepared to part-fund it, Mercuriadis (and HSM) can be free to hunt one other third-party backer’s cash.

If the HSF board chooses not to fireside Mercuriadis, in fact, the ‘name choice’ isn’t any menace to HSF. It stays in its field.

Step 5: Ah. However what if, following discontinuation, the HSF board de-lists Hipgnosis Songs Fund from the market, and sells it to, say, a serious music firm? The brand new house owners would kick Merck out!

That is the place issues get enjoyable.

Let’s think about precisely what you simply described occurs for actual. The board sells off Hipgnosis Songs Fund both at a worth that Hipgnosis Songs Capital/Blackstone is unwilling to match, or they by some means simply freeze out Merck Mercuriadis from the acquisition course of.

On this state of affairs, let’s say Universal, Sony, or Warner turns into the proprietor of HSF.

What would these firms naturally do on day one of proudly owning HSF? They’d sack Merck and HSM. Goodnight Vienna!

Besides that sacking… would then set off HSM’s ‘name choice’… which means that Mercuriadis and Blackstone would be capable of purchase HSM’s property off the brand new proprietor… with out that new proprietor having the ability to cease it.

A supply beforehand concerned in HSF at a senior degree instructed MBW earlier this week: “When issues have been going nice, 5 or so years in the past, the [HSF] board waved Merck’s ‘name choice’ request via with out fuss.

“It’s laughable that the identical board requested him to spike the identical ‘name choice’ the opposite week – and hardly stunning he instructed them no manner.”

“When issues have been going nice, 5 or so years in the past, the [HSF] board waved Merck’s ‘name choice’ request via with out fuss.”

MBW supply

Stated the identical supply: “Merck has all the time maintained that he made certain he crossed the t’s and dotted the i’s in order that when he instructed these songwriters he would symbolize their catalogs for the remainder of his life, he would.”

One other supply near Hipgnosis Songs Fund’s preliminary IPO in 2018 feedback, “Merck defined to shareholders in the beginning that if he was going to construct a multi-billion greenback fund, he’d have to navigate some very emotional discussions with songwriters. If he was going to accumulate catalogs from cultural giants like Neil Younger – and Neil Younger was the precise instance he used on the time – he’d need to make a deal for his or her ‘metaphorical youngsters’.

“That was the justification for his ‘name choice’: To [buy catalogs] straight from individuals like Neil Younger, Merck must look artists within the eye and promise them that he’d by no means have to surrender the administration of their songs, no matter whether or not the capital behind Hipgnosis ever modified.

“Shareholders agreed to Merck’s ‘name choice’ earlier than they ever invested a pound in Hipgnosis. It’s been within the firm’s prospectus spelled out since day one.”

Step 6: Couldn’t Hipgnosis Songs Fund get authorized? Attempt to weaken Merck’s ‘name choice’, or terminate HSM, that manner?

I imply, sure, in fact, they might all the time strive. And what a flurry of thrilling headlines that may deliver to MBW 😃!

However it could even be extraordinarily messy… and, assuming Mercuriadis has run his ship diligently, it could seemingly be unsuccessful.

There are boilerplate provisions in HSM’s settlement with HSF, as famous within the authentic HSF prospectus, that cowl HSM’s contract being terminated if HSM commits the standard standout fiscal sins (wilful misconduct, fraud, breaches of obligations and many others.).

There’s additionally a boilerplate clause in there about HSM having the ability to be chopped by HSF if there’s a ‘Key Individual Occasion’ (i.e. if Merck Mercuriadis can now not act as CEO of HSM).

However right here’s what we all know: (a) Mercuriadis’ ‘name choice’ has been a part of HSF’s prospectus earlier than anybody was requested to put money into the agency; and (b) That very same ‘name choice’ is clearly deemed rock strong sufficient for HSF’s board to publicly admit – previously few weeks – that they asked Mercuriadis to revoke it. (He mentioned no, obvs.)

Right here’s what else we all know: Hipgnosis Songs Fund, with a near-maxed-out RCF in a tricky rate of interest setting, most likely doesn’t have a barrel-load of money proper now for an enormous authorized battle (esp vs. an opponent doubtlessly funded by Blackstone).

In the end, a peaceable resolution will certainly be the popular consequence for all events.

As Mercuriadis mentioned in his assertion yesterday “… we stay up for working with a brand new Chair and reconstituted Board throughout this era to make sure that the Hipgnosis Songs Fund delivers for its shareholders“.

Step 7: Is That your intestine intuition? That HSM will stay adviser for HSF, working with a brand new board to shore up a share worth that’s plummeted? Even with HSF’s robust debt-payback vs. dividends stability to strike?

No, that’s not my intestine intuition.

Mercuriadis has said publicly that he want to see HSF shareholders profit from the capital development that can include HSF’s owned catalog in years to return. He’s additionally talked about his gratitude to these shareholders for making the institution of songs as an asset class potential.

No matter all that, my intestine intuition is that these shareholders will ultimately ask Mercuriadis/Blackstone to purchase Hipgnosis Songs Fund, or purchase the total HSF catalog, throughout the subsequent 12 months.

I’ve zero information of whether or not or not it will come to cross, or if such discussions have even been flirted with thus far.

It simply feels just like the neatest potential conclusion for all. It’s an consequence wherein everybody at the moment invested in HSF, both through shareholder fairness or sweat (HSM included), can stroll away with a level of satisfaction.

The worth for that deal, I’d guess, will fall someplace between HSF’s public share worth and the now-infamous ‘operative NAV’ (i.e. non-public valuation) placed on the HSF portfolio.

In March, that operative NAV stood at USD $2.316 billion.

Step 8: Your recommended consequence would certainly be a shock, although? Seeing as HSF shareholders simply voted overwhelmingly to reject Blackstone/HSC’s $440 million supply – which got here through Merck – to purchase 29 of HSF’s catalogs. The consensus is that Merck’s supply considerably under-valued these property, coming because it did at a 17.5% low cost in the marketplace price of the catalogs as per Citrin Cooperman’s estimate.

There’s an entire different article to be written about this, digging deeper into the ‘true’ a number of that Harmony is paying for HSF’s rival, Spherical Hill Royalty Fund Ltd (see details of that here) vs. the a number of implied by HSM’s $440 million supply.

However for now I’ll keep on with this: there’s a little bit of ‘having cake and consuming it’ about your factors.

For a while now, Hipgnosis Songs Fund’s unbiased valuer, Citrin Cooperman, has come in for flak (from these with a bearish view on Hipgnosis) for the 8.5% low cost charge utilized in CC’s valuations of HSF.

Regardless of price of capital and rates of interest leaping up and up, Citrin Cooperman (previously Massarsky Consulting) has resisted the concept of elevating that 8.5% to, say, 9% or 9.5%, at each flip.

There may be fierce debate on the market over this resolution: For instance, see Spherical Hill Royalty Fund Ltd’s use of a second valuer (FTI), along with Citrin Cooperman, when getting its personal valuation report done in April.

For a calculation to find out the Spherical Hill fund’s worth (for the aim of financing with financial institution debt), Citrin Cooperman caught with a reduction charge of 8.5%.

FTI, however, used the next low cost charge, of 9.25%.

(FTI used a decrease charge when calculating the fund’s price for ABS financing.)

Citrin Cooperman’s 8.5% low cost charge is without doubt one of the causes, says HSF critics, why there’s an such unhealthy gulf between Hipgnosis Songs Fund’s share worth/market cap and its ‘Operative NAV’ right this moment.

But if that 8.5% low cost charge went up, as some HSF critics recommend it ought to within the present fiscal setting, then as a direct consequence the unbiased worth of HSF would go down.

And on account of that, the now-rejected $440 million supply from Hipgnosis Songs Capital/Blackstone for the 29 catalogs of HSF would immediately look considerably rosier (vs. the re-valued price of HSF’s property).

Moreover, throughout HSF’s ‘go-shop’ interval, HSF’s board and monetary advisor JP Morgan couldn’t find any other party willing to raised HSC’s $440 million supply for the property.

That’s regardless of 17 firms having a bit kick of HSF’s tires initially of the ‘go-shop’ course of.

(Some sources recommend the ‘go-shop’ contained offputting ‘poison capsules’ for rival bidders vs. Blackstone’s $440 million supply, not least the truth that Blackstone/HSC had a ‘matching proper’ to gazump any third-party bid that got here ahead. Different sources near the ‘go-shop’, nonetheless, argue it was a respectable course of, and that within the music trade ‘matching rights’ are commonplace throughout the acquisition tender of enormous catalogs.)

Will HSF shareholders find yourself regretting that they handed on HSC/Blackstone’s $440 million supply – which equated to a a number of of 18.3x historic Internet Writer Share (NPS) of the catalogs in query?

Perhaps. Perhaps not. That each one relies on the place the general public worth of Hipgnosis Songs Fund strikes subsequent.

As issues stand, anticipate Merck Mercuriadis, with that all-important ‘name choice’ in his again pocket, to have a front-row seat for the following chapter on this story.

[ad_2]